Rolling Window Time Series Regression

Source:vignettes/Rolling_Window_Time_Series_Regression.Rmd

Rolling_Window_Time_Series_Regression.RmdIn this short tutorial, I show how to calculate a rolling regression

on grouped time series data using tidyfit. With very few

lines of code, we will be able to estimate and analyze a large number of

regressions. As usual, begin by loading necessary libraries:

library(dplyr); library(tidyr); library(purrr) # Data wrangling

library(ggplot2); library(stringr) # Plotting

library(lubridate) # Date calculations

library(tidyfit) # Model fittingThe data set consists monthly industry returns for 10 industries, as well as monthly factor returns for 5 Fama-French factors (data set is available here). The factors are:

- The market risk premium

Mkt-RF - Size

SMB(small minus big) - Value

HML(high minus low) - Profitability

RMW(robust minus weak) - Investment

CMA(conservative minus aggressive)

Returns are provided for 10 industries, and excess returns are calculated by subtracting the risk free rate from the monthly industry returns:

data <- Factor_Industry_Returns

data <- data |>

mutate(Date = ym(Date)) |> # Parse dates

mutate(Return = Return - RF) |> # Excess return

select(-RF)

data

#> # A tibble: 7,080 × 8

#> Date Industry Return `Mkt-RF` SMB HML RMW CMA

#> <date> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1963-07-01 NoDur -0.76 -0.39 -0.44 -0.89 0.68 -1.23

#> 2 1963-08-01 NoDur 4.64 5.07 -0.75 1.68 0.36 -0.34

#> 3 1963-09-01 NoDur -1.96 -1.57 -0.55 0.08 -0.71 0.29

#> 4 1963-10-01 NoDur 2.36 2.53 -1.37 -0.14 2.8 -2.02

#> 5 1963-11-01 NoDur -1.4 -0.85 -0.89 1.81 -0.51 2.31

#> 6 1963-12-01 NoDur 2.52 1.83 -2.07 -0.08 0.03 -0.04

#> 7 1964-01-01 NoDur 0.49 2.24 0.11 1.47 0.17 1.51

#> 8 1964-02-01 NoDur 1.61 1.54 0.3 2.74 -0.05 0.9

#> 9 1964-03-01 NoDur 2.77 1.41 1.36 3.36 -2.21 3.19

#> 10 1964-04-01 NoDur -0.77 0.1 -1.59 -0.58 -1.27 -1.04

#> # ℹ 7,070 more rowsThe aim of the analysis is to calculate rolling window factor betas using a regression for each industry. To fit a regression for each industry, we simply group the data:

data <- data |>

group_by(Industry)Let’s verify that this fits individual regressions:

mod_frame <- data |>

regress(Return ~ CMA + HML + `Mkt-RF` + RMW + SMB, m("lm"))

mod_frame

#> # A tibble: 10 × 7

#> Industry model estimator_fct `size (MB)` grid_id model_object settings

#> <chr> <chr> <chr> <dbl> <chr> <list> <list>

#> 1 Durbl lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 2 Enrgy lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 3 HiTec lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 4 Hlth lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 5 Manuf lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 6 NoDur lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 7 Other lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 8 Shops lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 9 Telcm lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 10 Utils lm stats::lm 0.496 #0010000 <tidyFit> <tibble>The model frame now contains 10 regressions estimated using

stats::lm. We may want to fit the regression using a

heteroscedasticity and autocorrelation consistent (HAC) estimate of the

covariance matrix, since we are working with financial time series. This

can be done by passing the additional argument to m(...):1

mod_frame_hac <- data |>

regress(Return ~ CMA + HML + `Mkt-RF` + RMW + SMB, m("lm", vcov. = "HAC"))

mod_frame_hac

#> # A tibble: 10 × 7

#> Industry model estimator_fct `size (MB)` grid_id model_object settings

#> <chr> <chr> <chr> <dbl> <chr> <list> <list>

#> 1 Durbl lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 2 Enrgy lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 3 HiTec lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 4 Hlth lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 5 Manuf lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 6 NoDur lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 7 Other lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 8 Shops lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 9 Telcm lm stats::lm 0.496 #0010000 <tidyFit> <tibble>

#> 10 Utils lm stats::lm 0.496 #0010000 <tidyFit> <tibble>A rolling window regression can be estimated by specifying an

appropriate cross validation method. tidyfit uses the

rsample package from the tidymodels suite to

create cross validation slices. Apart from the classic CV methods

(vfold, loo, expanding window, train/test split), this also includes

sliding functions (sliding_window,

sliding_index and sliding_period), as well as

bootstraps. The sliding functions do not generate a

validation slice, but only create rolling window training slices. We

will be using sliding_index, which works well with date

indices. See ?rsample::sliding_index for specifics.2

Since the method lm has no hyperparameters, it is not

passed to the cross validation loop by default, since this would create

unnecessary computational overhead. To ensure that models are fitted on

train slices, we need to add the additional argument

.force_cv = TRUE. Furthermore, the CV slices are typically

not returned but only used to select optimal hyperparameters. To return

slices set .return_slices = TRUE:

mod_frame_rolling <- data |>

regress(Return ~ CMA + HML + `Mkt-RF` + RMW + SMB,

m("lm", vcov. = "HAC"),

.cv = "sliding_index", .cv_args = list(lookback = years(5), step = 6, index = "Date"),

.force_cv = TRUE, .return_slices = TRUE)The .cv_args are arguments passed directly to

rsample::sliding_index. We are using a 5 year window

(lookback = years(5)), and skipping 6 months between each

window to reduce the number of models fitted

(step = 6).

The model frame now contains models for each slice for each industry.

The slice_id provides the valid date for the respective

slices. Betas can be extracted using the built-in coef

function:

df_beta <- coef(mod_frame_rolling)

df_beta

#> # A tibble: 6,480 × 6

#> # Groups: Industry, model [10]

#> Industry model term estimate slice_id model_info

#> <chr> <chr> <chr> <dbl> <chr> <list>

#> 1 Durbl lm (Intercept) -0.434 1968-07-01 <tibble [1 × 3]>

#> 2 Durbl lm CMA 0.0258 1968-07-01 <tibble [1 × 3]>

#> 3 Durbl lm HML 0.661 1968-07-01 <tibble [1 × 3]>

#> 4 Durbl lm Mkt-RF 1.28 1968-07-01 <tibble [1 × 3]>

#> 5 Durbl lm RMW 0.898 1968-07-01 <tibble [1 × 3]>

#> 6 Durbl lm SMB -0.150 1968-07-01 <tibble [1 × 3]>

#> 7 Durbl lm (Intercept) -0.423 1969-01-01 <tibble [1 × 3]>

#> 8 Durbl lm CMA 0.235 1969-01-01 <tibble [1 × 3]>

#> 9 Durbl lm HML 0.569 1969-01-01 <tibble [1 × 3]>

#> 10 Durbl lm Mkt-RF 1.25 1969-01-01 <tibble [1 × 3]>

#> # ℹ 6,470 more rowsIn order to plot the betas, we will add confidence bands. HAC

standard errors are nested in model_info in the

coefficients frame:

df_beta <- df_beta |>

unnest(model_info) |>

mutate(upper = estimate + 2 * std.error, lower = estimate - 2 * std.error)

df_beta

#> # A tibble: 6,480 × 10

#> # Groups: Industry, model [10]

#> Industry model term estimate slice_id std.error statistic p.value upper

#> <chr> <chr> <chr> <dbl> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 Durbl lm (Interce… -0.434 1968-07… 0.383 -1.13 2.62e- 1 0.332

#> 2 Durbl lm CMA 0.0258 1968-07… 0.262 0.0985 9.22e- 1 0.550

#> 3 Durbl lm HML 0.661 1968-07… 0.239 2.77 7.68e- 3 1.14

#> 4 Durbl lm Mkt-RF 1.28 1968-07… 0.124 10.3 2.00e-14 1.52

#> 5 Durbl lm RMW 0.898 1968-07… 0.378 2.37 2.11e- 2 1.65

#> 6 Durbl lm SMB -0.150 1968-07… 0.133 -1.13 2.65e- 1 0.116

#> 7 Durbl lm (Interce… -0.423 1969-01… 0.396 -1.07 2.90e- 1 0.369

#> 8 Durbl lm CMA 0.235 1969-01… 0.264 0.889 3.78e- 1 0.764

#> 9 Durbl lm HML 0.569 1969-01… 0.243 2.34 2.29e- 2 1.06

#> 10 Durbl lm Mkt-RF 1.25 1969-01… 0.150 8.33 2.52e-11 1.55

#> # ℹ 6,470 more rows

#> # ℹ 1 more variable: lower <dbl>Now, with all the pieces in place, we can plot the results. Let’s

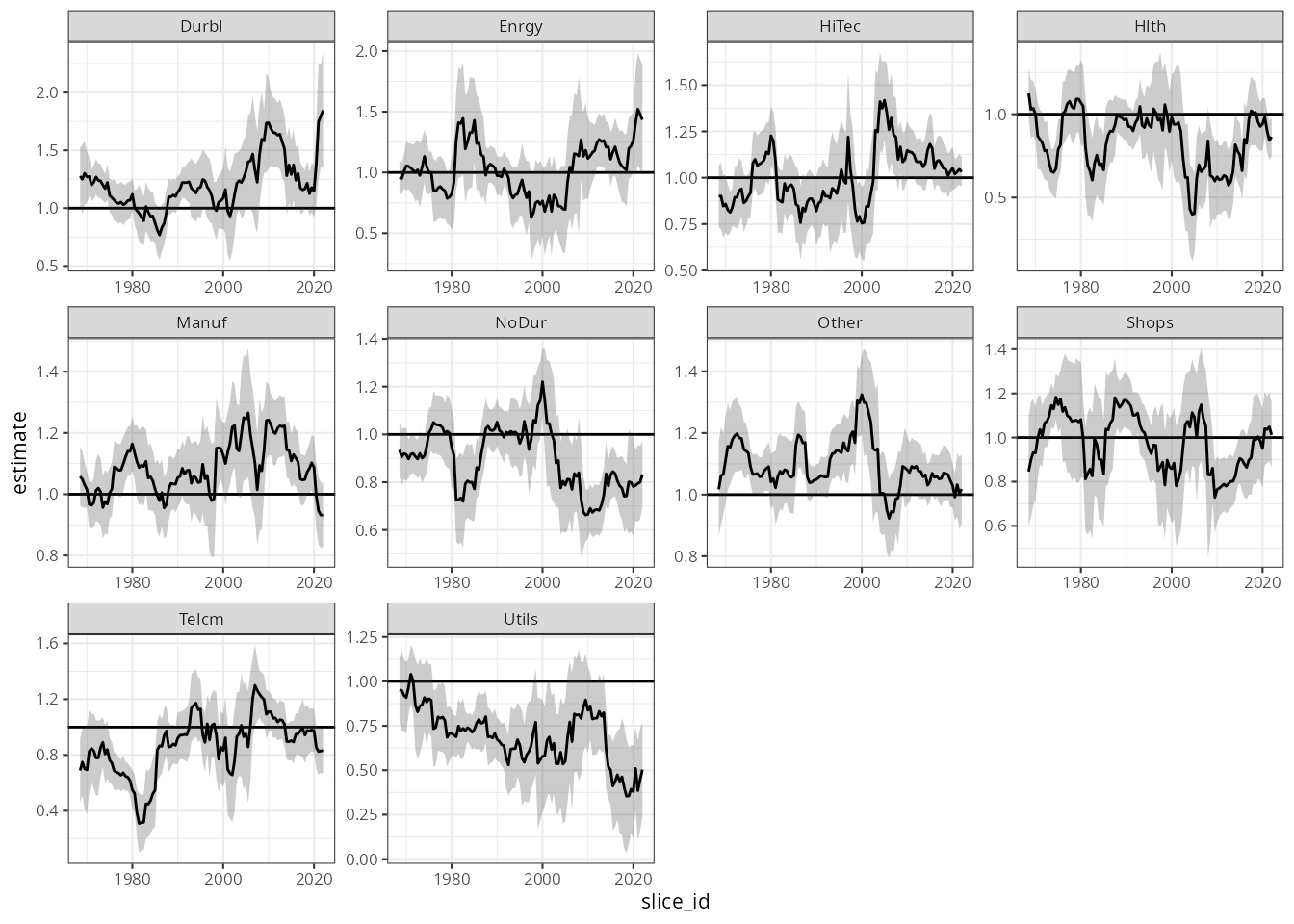

begin by examining the market beta for each industry using

ggplot2:

df_beta |>

mutate(slice_id = as.Date(slice_id)) |>

filter(term == "Mkt-RF") |>

ggplot(aes(slice_id)) +

geom_hline(yintercept = 1) +

facet_wrap("Industry", scales = "free") +

geom_ribbon(aes(ymax = upper, ymin = lower), alpha = 0.25) +

geom_line(aes(y = estimate)) +

theme_bw(8)

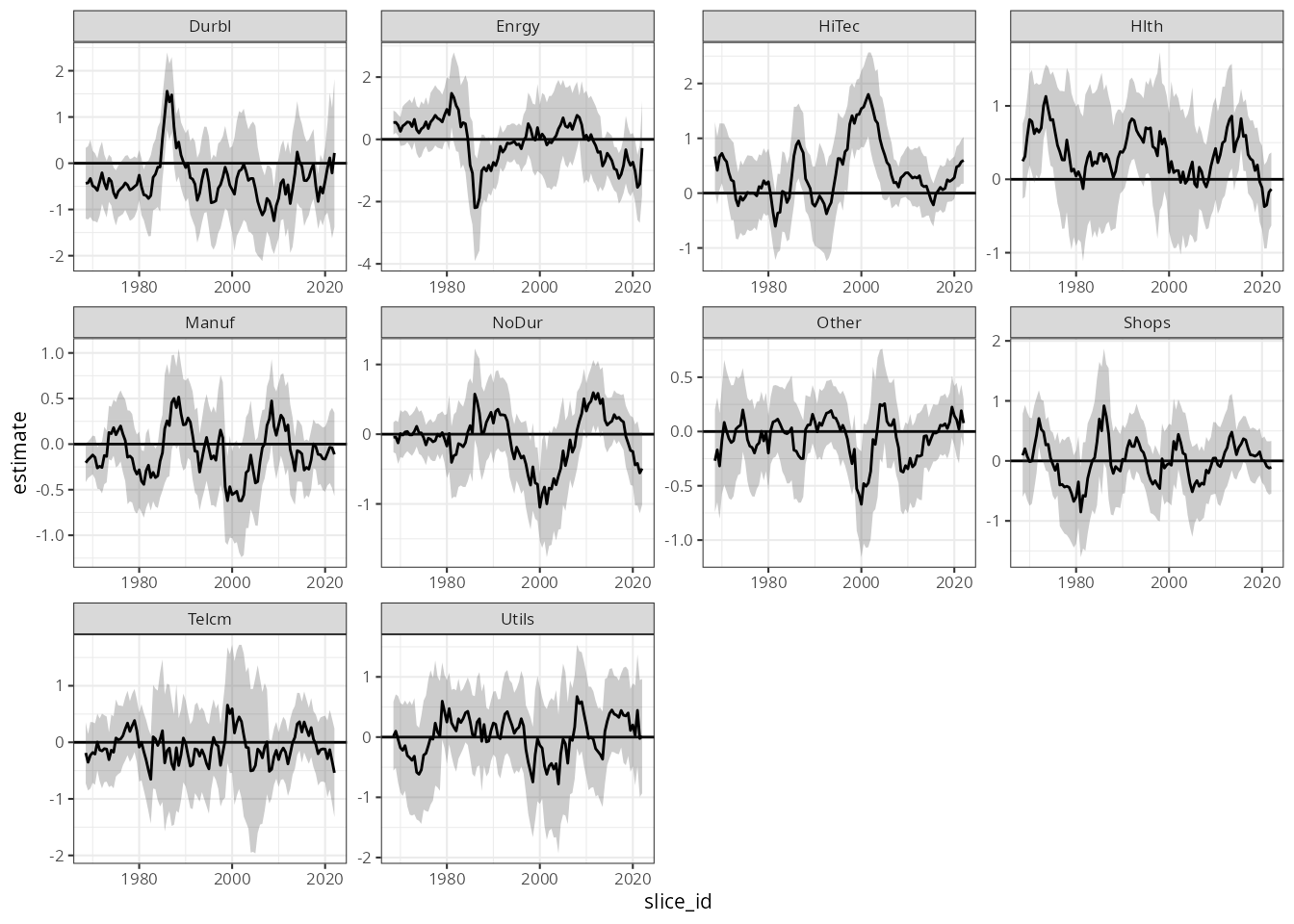

Or plotting risk-adjusted return (alpha) given by the intercept:

df_beta |>

mutate(slice_id = as.Date(slice_id)) |>

filter(term == "(Intercept)") |>

ggplot(aes(slice_id)) +

geom_hline(yintercept = 0) +

facet_wrap("Industry", scales = "free") +

geom_ribbon(aes(ymax = upper, ymin = lower), alpha = 0.25) +

geom_line(aes(y = estimate)) +

theme_bw(8)

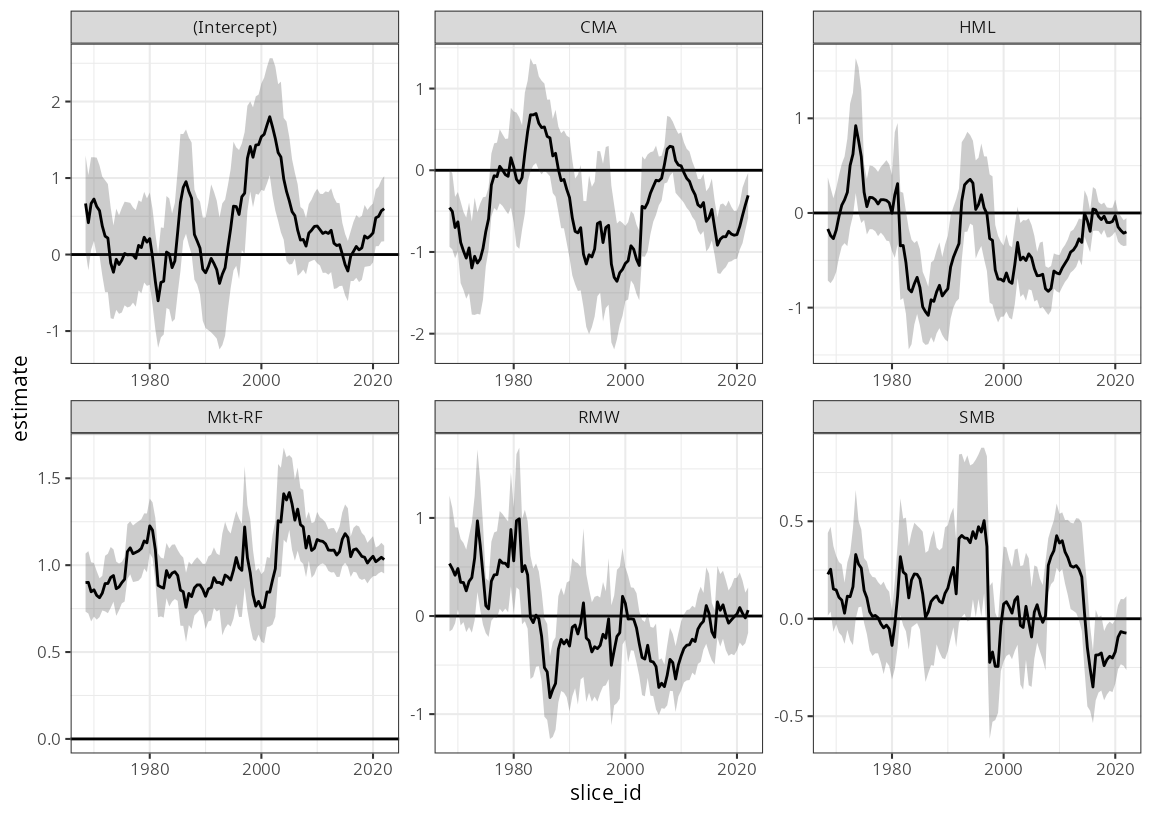

Or plotting all parameters for the HiTec industry:

df_beta |>

mutate(slice_id = as.Date(slice_id)) |>

filter(Industry == "HiTec") |>

ggplot(aes(slice_id)) +

geom_hline(yintercept = 0) +

facet_wrap("term", scales = "free") +

geom_ribbon(aes(ymax = upper, ymin = lower), alpha = 0.25) +

geom_line(aes(y = estimate)) +

theme_bw(8)

While there are certainly very interesting insights to be had here,

the aim of this walk-through is not to interpret these results, but

rather to demonstrate how a complex piece of analysis can be done very

efficiently using the tidyfit package.

In a follow-up article found here, I compare the results in the plot above to a time-varying parameter regression to show how more robust methods can be used to avoid window effects in the rolling sample and to shrink some coefficients to constant values.

Note that the

...inm()passes arguments to the underlying method (i.e.stats::lm). However in some casestidyfitadds convenience functions, such as the ability to pass avcov.argument as used incoeftestforlm.↩︎It is important to note that

sliding_indexcan not be used to select hyperparameters since no test slices are produced. To perform time series CV, use therolling_originsetting, which is similar, but produces train and test splits.↩︎